|

Richard Fuld Testimony to Congress on Lehman Brothers Bankruptcy delivered 6 October 2008, House Oversight and Reform Committee, Washington, D.C.

[AUTHENTICITY CERTIFIED: Text

version of Opening Statement transcribed directly from audio]

Mr. Fuld: Chairman Waxman, Ranking

Member Davis, and Members of this distinguished committee:

Today there is unprecedented turmoil in our capital

markets. Nobody, including me, anticipated how the problems that

started in the mortgage markets would spread to our credit markets,

and our banking system, and now threaten our entire financial system

and our country.

Like many other financial institutions,

Lehman Brothers got caught in

this financial tsunami. But I want to be very clear. I take full

responsibility for the decisions that I made and for the actions

that I took. Based on the information that we had at the time, I

believed that these decisions and actions were both prudent and

appropriate.

None of us ever gets the opportunity to turn back the

clock. But with the benefit of hindsight, would I have done things

differently? Yes, I would have. As painful as this is for all of the

people affected by the bankruptcy of Lehman Brothers, this is not

just about Lehman Brothers. These problems are not limited to Wall

Street, or even Main Street. This is a crisis for the global economy.

We live in a world where large investment

-- large

independent U.S. investment banks are now extinct, where

AIG and

Fannie Mae and Freddie Mac are under government control, and where

major institutions are being rescued, and where regulators are

engaged in a daily struggle to stabilize the financial system. In

this environment, it's not surprising that the media coverage of

Lehman's demise has been rife with rumors and inaccuracies. I

appreciate the opportunity to set the record straight for this

committee, and to be as helpful as possible in explaining why we

ultimately could not prevent a bankruptcy filing. And then I want to

respond to your questions.

I'm a Lehman lifer. I joined as an intern in 1966, and got a

full-time job as a

commercial paper trader while earning my business

degree at night. In 1994, when

Lehman Brothers was spun out of

American Express as a separate company and I became the CEO, we were

a small domestic bond firm. By 2007, we had built Lehman into a

diversified global firm with 28,000 employees. I feel a deep

personal connection to those 28,000 great people, many of whom have

dedicated their entire careers to Lehman Brothers. I feel horrible

about what has happened to the company and its effects on so many --

my colleagues, my shareholders, my creditors, and my clients.

As CEO, I was a significant shareholder, and my long-term

financial interests were completely aligned with those of all the

other shareholders. No one had more incentive to see Lehman Brothers

succeed. And because I believed so deeply in the company, I never

sold the vast majority of my Lehman Brothers stock, and still owned

10 million shares when we filed for bankruptcy.

As I said, following the spin-off of Lehman Brothers from

American Express, our business was almost exclusively at a fixed

income. We recognized the need for diversification, and over the

subsequent 14 years we built and acquired significant equity and

asset management businesses. We established a presence in 28

countries. We also continually strengthened our risk management

infrastructure.

Lehman Brothers did have a significant presence in the

mortgage market. This should not be surprising, though. U.S.

residential mortgages are an 11 trillion dollar market, more than twice

the size of the U.S. Treasury market, and a serious participant in

the fixed-income business, had a significant presence in the

mortgage market.

As the environment changed, we took numerous

actions to reduce our risk. We strengthened our balance sheet,

reduced leverage, improved liquidity, closed our mortgage

origination businesses, and reduced our exposure to troubled assets. We also raised over 10 billion dollars in new capital. We explored

converting to a back -- a bank holding company. We looked at a wide range of

strategic alternatives, including spinning off our commercial real

estate assets to our shareholders.

We also considered selling part or all of the company. We

approached many potential investors, but in a market paralyzed by a

crisis in confidence

none of these discussions came to fruition.

Indeed, contrary to what you may have read, I never turned down an

offer to buy Lehman Brothers. Throughout 2008, the SEC and the

Federal Reserve conducted regular, and at times daily, oversight of

our business and our balance sheet. They saw what we saw in real

time as they reviewed our liquidity and our funding, our capital

risk management and our

mark-to-market process.

As the crisis in confidence spread throughout the capital

markets, naked short sellers targeted financial institutions and

spread rumors and false information. The impact of this market

manipulation became self-fulfilling. As short sellers drove down the

stock prices of financial firms, the rating agencies lowered their

ratings because lower stock prices made it harder to raise capital

and reduced financial flexibility. The downgrades in turn caused

lenders and counter parties to reduce credit lines and then demand

more collateral, which increased liquidity pressures.

At Lehman Brothers, the crisis in confidence that permeated

the markets led to an extraordinary run on the bank. In the end,

despite all of our efforts, we were overwhelmed. However, what

happened to Lehman Brothers could have happened to any financial

institution, and almost did happen to others. Bear Stearns, Fannie

Mae, Freddie Mac, AIG, Washington Mutual, and Merrill Lynch all were

trapped in this vicious cycle. Morgan Stanley and Goldman Sachs also

came under attack.

Lehman's demise was brought on by many destabilizing

factors: the collapse of the real estate market, naked short

attacks, false rumors, widening spreads on credit default swaps,

rating agency downgrades, a loss of confidence by clients and

counter parties, and buyers sitting on the sidelines waiting for an

assisted deal. Again, this is not just a Lehman Brothers story. It's

now an all-too-familiar tale. It is to late for Lehman Brothers,

but the government has now been forced to dramatically

change the rules and provide substantial support to other

institutions.

I greatly

appreciate the opportunity to speak with you today; and if I can be

helpful to this committee,

in any way,

to understand how we got here

and what our country can do to move forward, I am happy to do so.

Thank

you, sir.

[authentication in process]

Chairman Waxman: Thank you very much,

Mr. Fuld. Without objection, the Chair and the ranking member will

control 10 minutes which they can use or reserve and use at a

subsequent time. Hearing no objection, that will be the order.

The Chair will recognize himself.

Mr. Fuld, the committee --

our committee -- requested

all the documents relating to your salary, bonuses and stock sales;

and the committee staff put together a chart, which I hope will come

up on the screen.

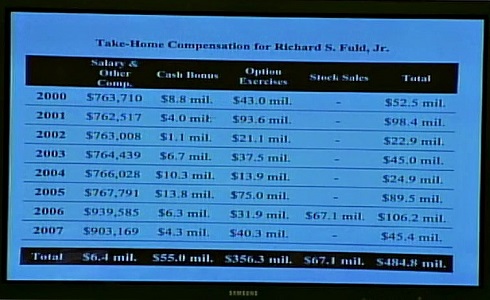

This chart will show your compensation for the

last 8 years. It shows your base salary, your cash bonuses and your

stock sales. In 2000, you received over 52

million dollars. In 2001, that increased to 98 million

dollars. It dipped for a few

years. And then in 2005, you took home 89 million dollars. In 2006, you

made a huge stock sale, and you received over 100 million dollars in that

year alone. Are these figures basically accurate?

Mr. Fuld: Sir, if those are the

documents that we provided to you, I would assume they are.

Chairman Waxman: Okay. The bottom line

is that, since 2000, you have taken home more than 480 million

dollars.

That's almost half a billion dollars,

and that's difficult to

comprehend for a lot of people. Your company is now bankrupt;

our economy is in a state of crisis;

but you get to keep 480

million dollars. I -- I

have a very basic question for you: Is this fair?

Mr. Fuld: Mr. Chairman, your first

question was about this slide: Are those numbers accurate? They are

accurate the way you have put them up on that slide, but

-- I believe your

number of cash and salary bonuses are accurate. The option exercises

-- the way you have them portrayed here I believe represent the full

option without the

strike price. And the only reason I exercised

those options was because they came due at maturity. If I had not exercised those, I would

have lost it. There was that stock sale, but --

Chairman Waxman:

Well...I'll leave

the record open for you to give me any changes in that list.

Mr. Fuld: What I would say to you --

Chairman Waxman: But, basically,

didn't you take home around 4 to 500

million dollars as the head of

Lehman Brothers for the last -- since 2000 to now?

Mr. Fuld: The majority of my stocks,

sir, came -- excuse me -- the majority of my compensation came in

stock. The vast majority of the stock that I got I still owned at

the point of our filing.

Chairman Waxman: The stock is in

addition to the numbers that I've indicated,

because those were

your salary and your bonuses. Now, you had bonuses; and, in addition

to that, you had some stock sales. You've lost some money of the

stock that you've received as compensation, which you received as

compensation on top of these other figures. So you've been able to

pocket close to half a [billion] dollars. And my question to you is, a

lot of people ask, "Is that fair for the CEO of a company that's now

bankrupt to have made that kind of money?" It's just

unimaginable to so many people.

Mr. Fuld: I would say to you the

500 [million dollars] number is not accurate. I would say to you that, although it's

still a large number, I think for the years that you're talking

about here, I believe my cash compensation was close to 60 million,

which you have indicated here. And I believe the amount that I took

out of the company over and above that was, I believe, a little bit

less than 250 million. Still a large number, though.

Chairman Waxman: Still a large amount

of money. You have a 14 million dollar ocean front home in Florida. You

have a summer vacation home in Sun Valley, Idaho. Yet you and your

wife have an art collection filled with million dollar paintings.

Your former President, Joe Gregory, used to travel to work in his

own private helicopter. I guess people wonder, if you made all this

money by taking risks with other people's money, you could have done

other things. You had high leverage, 30 to 1 and higher. You didn't

pay out billions of dollars in dividends. And you didn't have to pay

out these millions of dollars in dividends and bonuses. You could

have saved some of these funds for lean times, but you didn't.

Do you think it's fair and do you

have any recommendations on fundamental reforms that would bring a

new approach to executive compensation? Because it seems that the

system worked for you, but it didn't seem to work for the rest of

the country and the taxpayers who now have to pay up to 700 billion

dollars to bail out our economy.

You can't -- We can't continue to have a system

where Wall Street executives privatize all the gains and then

socialize the losses. Accountability needs to be a two-way street.

Do you disagree with that? And do you have any recommendations of

what we ought to be

doing in this area?

Mr. Fuld: Mr. Chairman, we had a

compensation committee that spent a tremendous amount of time making

sure that the interests of the executives and the employees were

aligned with shareholders. My employees owned close to 30 percent of

our company,

and that was because we wanted them to think, act,

and

behave like shareholders. When the company did well, we did well.

When the company did not do well, sir, we did not do well.

Chairman Waxman: Well, Mr. Fuld, there

seems to be a breakdown. Because you did very well when the company

was doing well and you did very well when the company wasn't doing

well. And now your shareholders who owned your company have

nothing. They've

been wiped out. I'm going to reserve the balance

of my time, and we're going to go on to other Members.

Mr. Fuld: The compensation committee

is now appointed by the corporate governance committee of the board.

Mr. Shays:

Yeah,

but

-- but

did you have a major

role in appointing the compensation committee?

Mr. Fuld: I believe I had more of a

role in the early or mid-'90's;

clearly less of a role these last

number of years.

Mr. Shays:

Yeah, and then, finally, of the

10 million shares that you had

-- had

in the company -- that's what you

have right now, 10 million shares?

Mr. Fuld: No. I don't have the exact

amount. I think it's closer to

eight

million shares, and that does not

include the options that expired

worthless. Well, actually,

they haven't expired -- that are still there with a longer term

vesting but with a much higher strike price than, obviously, where

the stock is today.

Mr. Shays: Thank you. Thank you, Mr.

Chairman.

Chairman Waxman: Thank you, Mr. Shays.

I want to recognize

Ms. Maloney for

five

minutes.

Yet

this report in the New York Times

-- and I'd like permission to have it referenced or put in the

record --

Chairman Waxman:: Without objection.

Ms.

Maloney:

--

last Friday, called

the

"Agency['s]

'04 Rule Let Banks Pile Up New Debt."

And many people

feel that this was a major cause of the crisis, and they reference a

meeting in April

of

2004. And I'd like to ask you, were you at that

meeting? Did you lobby for this change? Why did Lehman want to

increase its leverage? And, in hindsight, do you think the SEC rule

-- that changing this SEC rule was appropriate for protecting safety

and soundness, the stability of our markets, and -- and taxpayers'

money.

Mr. Fuld: Congresswoman, I was not at

that meeting, I believe, in 2004. And I do not recall if any other

of my people were there. I had a chance to -- while I was sitting in

the waiting room, I saw, I would assume, almost all of the first

panel. The information about leverage, I think, has been grossly

misunderstood. There are two numbers. One is gross leverage, and one

is net leverage. Gross leverage includes -- excuse me if I get

technical. If I get too technical, please stop me.

Close to half of our balance sheet, if

not more, was what we called the

matched book. The match book was

predominantly government securities and agencies that we took on our

balance sheet to finance for our clients. We were one of the top

U.S. Treasury Government traders and financiers, meaning financing

the U.S. Government debt. And we supplied a tremendous amount of

liquidity to institutional investors that owned U.S. Government debt

and agencies. At times, that was as high as 300 to probably more,

300 billion dollars. I heard some of the earlier remarks about if you lost

three or four percent of that. For the matched book, you do not -- those

are government securities. So the real number, the effective number,

is net leverage.

Ms. Maloney: So did you...lobby for

this capital rule change? And do you think it -- it contributed to the

financial instability and loss of safety and soundness in financial

institutions such as your own that allowed this increased leverage?

Mr. Fuld: I myself did not lobby for

the increased leverage.

Ms. Maloney: Did

-- Did Lehman Brothers

lobby for it?

Mr. Fuld: I'm not aware of that.

Ms. Maloney: I...would like to ask you,

now that we have the opportunity of looking back, and...we want to

look forward on what needs to be done, if you had to give government

advice on how we could strengthen the safety and soundness of our

institutions and the accountability and transparency that all of us

want, what would you recommend -- to change the system?

Mr. Fuld: In my written testimony, I

spoke about the need for additional regulation and new regulation, because when the original regulations were written, it was a very

different environment. I believe there were 10 million shares a day

traded, and today there are close to five billion shares traded. The

electronic connectivity today, not only within this country but

country to country; investors today, given that electronic

connectivity, have the right to move their money to the highest

returning asset, and money moves very quickly and freely.

So it's not just about regulation

within the US. I believe it's also about more of a

matrix regulation that is more global in nature. I would focus also

on capital requirements, capital requirements meaning more capital

for less liquid assets, and a more robust understanding of mark to

market, which, I believe, is one of the pillars of the new plan. Mark

to market during periods of stress create one set of numbers and

obviously, in a functioning noncredit crisis environment, produce

another set of numbers --

Chairman Waxman: Thank you.

Your prepared statement, which has these recommendations, are in the

record and we want to move on to other questioners. Do you want to

add one last point?

Mr. Fuld: Yes, please. And the other [set of numbers] is, something

I strongly believe in, is the creation of what I call a master

netting system, where all capital market counterparties download

each night all their transactions to one local spot, first in the

US and then eventually, hopefully, make that be global.

That's about all transactions and trades. It's about positions. It's about capital. It's about leverage.

[Excuse me (clearing throat).] And it would give whatever

regulator is then in control of that master netting system a

complete view of the financial landscape, the available capital to

each and every asset class, flexibility within those asset classes,

and vulnerability within those asset classes, and vulnerability of

one institution versus the next. What I am proposing is clearly

expensive, costly, but by comparison to the unprecedented regulation

this Congress has just passed, it is a fraction and, I believe,

money well spent. Chairman Waxman: Thank you. Mr. Mica for five minutes.

Mr. Mica: Thank you. Thank you, Mr. Chairman. And looking at, first, your comment on Lehman Brothers primarily dealing in some, for most of its history -- Mr. Fuld: Sir, I apologize, I cannot hear you. I'm sorry. Mr. Mica: Can you hear me now? Mr. Fuld: Yes, thank you. Mr. Mica: Again, when you opened your statement, you said that Lehman Brothers, and it was around for what, 150 years, dealt in some pretty hard assets and some secure investments. You've been around awhile. What -- What turned the corner for you to get into some of the more speculative ventures like subprime and some of the other, again, riskier investments? Mr. Fuld: As I said in my verbal testimony, our participation in the -- in the mortgage-related businesses was clearly a natural for us, given our dominance in fixed income. That was something that went back a number of years. And even as I listened, as I say, to the panel before me, they correctly pointed out that this was a goal of the government, to provide funding and mortgages to a number of people that typically would not or could not have received a mortgage. Mr. Mica: And -- And one of your big -- well, one of the big packagers or the competitors so to speak was Fannie Mae, which was deep into this. And you were -- you were dealing in some of the paper I think for secondary markets and other securitized mortgage paper to -- to basically package it, make money off it. Is that right? Mr. Fuld: Yes, sir.

Mr. Mica: Okay. What -- What was Lehman Brothers' exposure to the

debt of Fannie Mae and Freddie Mac, and what role did their collapse

play in precipitating some of your financial troubles? If it didn't

matter -- Mr. Mica: Okay. But their collapse, did that help precipitate any problems with your firm? Mr. Fuld: It certainly set the stage for an environment, as I talked about, loss of confidence and credit crisis mentality, that permeated our market; clearly set -- set the stage for investors losing confidence, counterparties asking for additional collateral, and clearly an environment that lost liquidity, which is the life blood of a capital market system. Mr. Mica: I noticed some questions were asked about your political participation. I pulled Lehman Brothers' contributions to Federal candidates for the last 10 years. Fortunately, I didn't find my name there but -- not like some of the other Members of Congress. I added some of this up. It's about 300,000 dollars that you gave to influence Members of Congress. Now, I also got your personal, which wasn't much, you probably bet a little bit too much on Hillary, too. But this is -- this is pretty much the extent of your financial contributions to Members of Congress, to lobby? Mr. Fuld: I believe that that was a result of Lehman's PAC -- Mr. Mica: Right. Mr. Fuld: -- which was not corporate moneys. Mr. Mica: Right, right. I am just telling you. But wait -- wait until you hear this one. And if you haven't discovered your role, you're the villain today. So you gotta act like the villain here. But guess what Fannie Mae did in the same period of time: 175 million dollars in lobbying contracts over 10 years. Does that surprise you? You were outlobbied. It sounds like rather than just some greed on Wall Street, we had a little greed in Washington. What would you say to that? Mr. Fuld: I think that's more a matter for your committee, sir.

Mr. Mica: Well, I hope -- I hope we get to it. Thank you. Chairman Waxman: The gentleman's time has expired. We now go to Mr. Cummings.

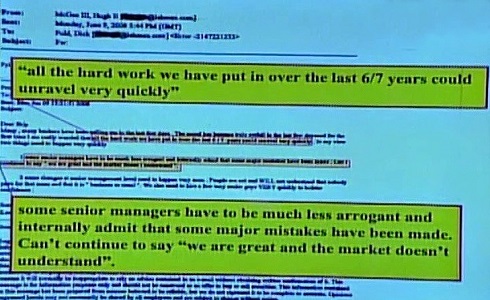

Mr. Cummings: Thank you very much, Mr. Chairman. Mr. Fuld, I really appreciate that you began your testimony by taking full responsibility for the company's downfall, which occurred on your watch. But there are some concerns that I want to -- to get to. As you know, the American taxpayer, many of them our constituents, just -- we just passed legislation giving 700 billion dollars to rescue Wall Street. One complaint I've heard over and over again from my constituents was that there seems to be a complete lack of accountability. They see Wall Street executives like you walking away with millions of dollars. And it's very interesting when you were talking about the chart that Mr. Waxman was -- showed you on the board, you said that it was inaccurate. But I'm going to discount it for you, and instead of $448 million over 8 years, let's say $350. How about that? $350. Is that okay? Can we discount it a little bit? You said it was not accurate. What would you say is accurate? Mr. Fuld: I'd say that's closer, sir. Mr. Cummings: Okay. I want to ask you about one of the e-mails obtained by the committee. On June 9th, 2008, a former top Lehman executive -- Can you hear me okay? Mr. Fuld: Yes, sir. Mr. Cummings: Benoit D'Angelin sent an e-mail to Hugh McGee, who was the global head of investment banking at Lehman. The e-mail says that many bankers have been calling in the last few days, and the mood has become truly awful.

It warns that (and I quote), "all the hard work we have put in...could unravel very quickly" (and of quote). And it offers the following advice. It says, "some senior managers have to be much less arrogant and internally admit that major mistakes have been made. [We] can't continue to say 'we are great, and the market doesn't understand'" (end of quote). Mr. McGee forwarded this e-mail to you on the same day and explained that it was representative of many others. When you read the e-mail, and this is interesting, what was your reaction? I am just curious. Mr. Fuld: I'm sorry, sir, what was the date of that? I'm sorry. Mr. Cummings: That would be June 9th, 2008. You -- You remember that e-mail? Mr. Fuld: I do not -- [first pass authentication verified to here (34:48)] Mr. Cummings: Well let me try to refresh your recollection a little bit. Let me tell you what you did, since you don't remember the e-mail. Here is what happened. You didn't take any personal responsibility. Instead, three days later, Mr. Fuld, on June 12th, you fired Erin Callan, your chief financial officer, and Joseph Gregory, your chief operating officer, but you stayed on and admitted no mistakes. You were CEO. Why didn't you take responsibility? Like today, you said you took full responsibility, why didn't you take responsibility for Lehman's mistakes? Why did you continue to say, "we are great, and the market doesn't understand?" In your testimony today, right here, right now, you continue to deflect personal responsibility. You cite what you call a litany of reasons for Lehman's bankruptcy. Mr. Fuld, I want to ask you about your personal responsibility, since you have taken it. Do you agree that Lehman took on excessive leverage under your leadership? Please answer yes or no. Mr. Fuld: It is not that easy. I will say to you, our leverage at times was higher, but as we entered this more difficult market over this last year, we continued to bring our leverage down so that even at the point, Congressman, on September 10th, when we announced our third quarter results, we had grossly reduced our balance sheet by close to $200 billion, specifically around residential mortgages and commercial real estate and leverage loans. Mr. Cummings: Mr. Fuld, I have only got about less than a minute. I have to get this question in. I assume your answer is no. I am just giving you the benefit of the doubt. Mr. Fuld: At the end of the day, we worked hard; our leverage was way down. One of the best leverage ratios on the street. And our tier one capital was one of the highest. Mr. Cummings: So you feel comfortable with what you did. Is that right? That is not one of the things that you said your -- Mr. Fuld: Yes, sir. Mr. Cummings: Okay, fine. Do you regret spending $10 billion in Lehman's cash reserves on bonuses, stock dividends, and stock buybacks as your firm faced a liquidity crisis? Do you regret that now? Mr. Fuld: I heard some of that while I was in the other room. I think that is a misunderstanding which I would like to clear up. Mr. Cummings: Well, let me go back to -- you go ahead, I am sorry. Mr. Fuld: Because it is important that this committee understands exactly what that was. When I talked about my employees owning close to 30 percent, what is typical of Wall Street is you take a percentage of your revenues and you pay your people. We asked our employees to take a big percentage of their compensation in stock. And so what that $10 billion was -- we had close to $19 billion of revenues -- what most of that $10 billion was, was compensation to our employees that they received in stock with a 5-year forward vest. So they didn't get that stock until 5 years, which aligned our interests, "our" being employees, with the interests of shareholders. To avoid dilution, because we took that $10 billion, gave it to the employees in stock, we had to take the $10 billion that they didn't get and go back into the open marketplace and buy back that stock so that we did not dilute our shareholders. And we did it each and every year. From where you sit, it looks like we just spent an extra $10 billion. That is not, sir, what we did. Mr. Cummings: Thank you very much, Mr. Chairman.

Chairman Waxman: It sounds like, though, and I yield myself time here, that you were trying to not to dilute the payment to those employees while you were in a liquidity crisis. Wouldn't it have made more sense to use that money to pay off the debts that were heavily on your shoulders at that point and you knew that you were in a difficult situation? Mr. Fuld: At that time, at the end of the year, last year, I didn't believe that we had that problem. Chairman Waxman: You didn't believe you had a liquidity problem. Mr. Fuld: And we did not have a liquidity problem at the end of last year. We had just completed a record year, none of which, by the way, came from mortgages. And we paid our people fairly and what we thought was competitive with the rest of the Street. Chairman Waxman: Okay. I accept your answer that you didn't think you had a liquidity problem, so you were trying to make sure that your employees were fully compensated. Mr. Fuld: Yes, sir. Chairman Waxman: Okay. Thanks. Mr. Turner. Mr. Turner: Thank you, Mr. Chairman. Mr. Fuld, in looking at your written testimony, you say ultimately what happened to Lehman Brothers was caused by a lack of confidence. I have a different view, and I have a couple questions for you about what it really comes down to is we are hearing that the subprime crisis, the predatory lending crisis, the mortgage foreclosure crisis. You said you listened to the first panel and their testimony. I am going to summarize it for you briefly. Mr. Fuld: I heard most of it, but yes, sir. Mr. Turner: They said there was a period of easy credit; that housing prices were escalating and then declined; that there was securitization of mortgages; that houses became like ATMs where people withdrew their equity; and excessive CEO compensation. That is not necessarily our experience in Ohio. Mr. Fuld: I am sorry, that is not what? Mr. Turner: That is not necessarily our experience in Ohio. In 2001, my community held a series of hearings on then subprime lending, predatory lending at the behest of City Commissioner Dean Lovelace. And we found that, in many instances, what we were seeing in the escalation of foreclosures was a result of inflated property values at the time of loan origination. In fact, we then turned to the Miami Valley Fair Housing Center in our community, an agency that was helping people who were in the foreclosure crisis, and Jim McCarthy from there reports that over 90 percent of the people that they were dealing with were actually refinances and that many of them had issues of the original value of the property at the time of refinancing where the property values were inflated. Now, clearly, we are in a period now of decline or slow growth in some areas which is compounding the problem, but I think people are getting off too easy when we say that declining property values are the problem. And I want to tell you what my concern here is. I believe that if you issue a loan at origination where the loan value exceeds the property value and that you then issue securities based upon that loan and you don't disclose that gap that existed at loan origination, that you are in fact, I believe, stealing. I believe that we are in a series of situations where people aren't disclosing that at loan origination, in fact, there was already a gap between value and loan amount, and that the declining house values really just emphasize it and compound it. So I have two questions for you. The first is, do you believe that if mortgage-backed securities are issued and they do not disclose at origination that the original loan amount exceeds the property value, that it is stealing? And second, would you please describe Lehman Brothers' role in both issuing subprime loans and mortgage-backed securities? Mr. Fuld: I do not believe that any of the original mortgage securitizers knowingly at the point of origination would have taken a mortgage whose value was in excess of the value of the home. I find that very difficult to either understand or believe. Mr. Turner: And if it occurred? Mr. Fuld: If it did occur, I would say it was lack of understanding of what the real value was. But I don't think -- I can't talk for the world in general, clearly, but highly unlikely that anybody would do that purposely. Mr. Turner: Then could you go to the role of your company in actually issuing original loans and then mortgage-backed securities? Mr. Fuld: We actually owned a number of what we called origination platforms. But those were more wholesale, where we went around to individual groups or companies of brokers that did in fact originate loans. When we bought them, we changed management, we changed underwriting standards to make them much more restrictive, to improve the quality of the loans that we did in fact originate so that those loans that we did then put into securitized form would be solid investments for investors. Mr. Turner: So then would it be your testimony that none of those original loans that were issued by your company exceeded the property value at origination? Mr. Fuld: Congressman, in all fairness, I did not review each and every loan. I must tell you the truth on that, I did not. And it would be a misstatement for me to say that -- Mr. Turner: I thought I had heard you say that no one would do that. And I tell you the experience in Ohio is that is exactly what was being done. Mr. Fuld: I would say no one would do it knowingly. Mr. Turner: Since you were at the top of the organization, I really wanted to get your perspective of how something like that could be happening. As I go through neighborhoods in Ohio and see abandoned house after abandoned house, where so many times the American dream of having a home have been stolen from people in refinancing where they did not understand the transaction they were in, and where the value at origination was inflated, making them captive to the house, ultimately leading to foreclosure. Mr. Fuld: Let me clarify that if I can. I said nobody would knowingly do that. Mr. Turner: Thank you, Mr. Chairman.

Chairman Waxman: Thank you, Mr. Turner. Mr. Kucinich. Mr. Kucinich: Thank you. I want to associate myself with the remarks and questions of my colleague from Ohio. Mr. Fuld, I have here a copy of a memo from April 12, 2008, that you sent to -- it is an e-mail that you sent to Thomas Russo. It says you just finished the Paulson dinner. This is a memo -- did you have dinner with Mr. Paulson back in April? Mr. Fuld: I very easily could have, sir. Mr. Kucinich: This memo references it. Mr. Fuld: I don't believe it was just the two of us. Mr. Kucinich: But did you meet with him? Mr. Fuld: You are asking me specifically on that date? Mr. Kucinich: Did you talk to Mr. Paulson on a regular basis? Mr. Fuld: We had a number of conversations, sir. Mr. Kucinich: Okay. Now, would you tell me, this memo says, that you sent to your colleagues, that we have a huge brand with Treasury. Speaking of Treasury, loved our capital raise. Do you feel at any time in this process that Mr. Paulson misled you? Mr. Fuld: I am sorry, sir, in response to this -- Mr. Kucinich: Do you feel at any time in these conversations -- we have your telephone logs -- that you were misled by the Treasury Secretary? Mr. Fuld: No, sir, I do not. Mr. Kucinich: And do you feel then -- you know, on September 10th, you had a conference call with your investors. During the conference call, your investors were told no new capital would be needed; that Lehman's real estate investment property -- investments were properly valued. Five days later, you filed for bankruptcy. Did you mislead your investors? And I remind you, sir, you are under oath. Mr. Fuld: No, sir. We did not mislead our investors. And to the best of my ability at the time, given the information that I had, we made disclosures that we fully believed were accurate. And I should -- and I should -- Mr. Kucinich: I want to go back to something here. You know, you have a memo here where you say that Secretary Paulson wanted to implement minimum capital standards, leverage standards, and liquidity standards. These seem to be some of the things that got your company in so much trouble. Now, did he ever tell you in all the conversations you had with him that he decided not to implement any of the proposals he discussed with you last April? And does any part of you feel that you were double crossed by the Secretary and he was playing you off against let's say Goldman Sachs? Mr. Fuld: I would sincerely hope that was not the case. Mr. Kucinich: And what about these things that he said to you about minimum capital standards, leverage standards, liquidity standards? Did he ever tell you he decided not to implement any of these things? You talked to him on a regular basis. What can you tell this subcommittee to enlighten us about where Secretary Paulson was? And you, as the head of Lehman Brothers, did you rely on anything that he told you that could have put Lehman Brothers down? Mr. Fuld: We instituted ourselves our own plan for reducing leverage, our own plan for increasing liquidity. And I will note that, on September 10th, when we pre- announced our earnings, we had $41 billion of excess liquidity. Mr. Kucinich: Let me ask you this, when did you know that J.P. Morgan was going to make a $5 billion collateral call? When did you first know about that? Mr. Fuld: I know that they had had conversations with our Treasury people. Mr. Kucinich: When? Mr. Fuld: I am not sure of the date. But it was -- Mr. Kucinich: Mr. Chairman, if I may -- thank you, sir, you are not sure. Mr. Chairman, this is a central question here, because with J.P. Morgan making a $5 billion collateral call, and on September 10th, they were telling investors they didn't have any more need for capital, that the real estate investments were properly valued, this puts us in a position where one of two things is possible. Either they were lying to their investors or they were misled by Secretary Paulson as to what could be done to help you, because after that 5 billion collateral call, that is what led directly to Lehman Brothers going down. Isn't that correct? Didn't you go down right after you understood that they were not going to remove that collateral call? Mr. Fuld: When you say collateral call, that is not the same thing as a margin call. Mr. Kucinich: I am talking about a collateral call. Mr. Fuld: No, I know. But the collateral call was not to meet a deficit in collateral that they were holding to offset risk. The collateral call, I believe, was because, as our clearing bank, they just asked for additional collateral to continue to clear for us. Mr. Kucinich: Thank you. Thank you, Mr. Chairman. Thank you, Mr. Fuld.

Chairman Waxman: The gentleman's time has expired. Mr. Tierney. Mr. Fuld: Excuse me, I should clarify also, sir, I didn't mean to cut you off there. This is probably a subject for litigation, and it is probably appropriate that I leave it to that. I believe the creditors and J.P. Morgan are having a conversation. Mr. Kucinich: Indeed. Indeed. Chairman Waxman: Mr. Tierney. Mr. Tierney: Mr. Fuld, thank you for joining us here this afternoon. Just before Lehman went into bankruptcy, you were in conversations with the Korean Development Bank, which I believe is a South Korean lender. What amount of money were you looking for them to contribute to Lehman? Mr. Fuld: Congressman, our conversations with KDB, as one of five banks in a consortium, stretched over a number of months. Mr. Tierney: Can you tell me the amount that you were looking for from the consortium? Mr. Fuld: It wasn't so much that we were looking from them. Their original proposal was they wanted to buy in the open market close to 50 percent of our stock. It was not about giving us new capital. They wanted to buy close to 50 percent. Mr. Tierney: And was that type of arrangement something that you were looking for at that time? Mr. Fuld: I would have welcomed that transaction, yes, sir. Mr. Tierney: Okay. Now, at about that time, in looking for that kind of transaction, you knew, because you had known for some time that you were already in a precarious situation. And I say that because there were reports that as far back as Christmas of 2006 that you were telling people that you had a cautious outlook for the year ahead. The next month in January, when you were in Davos at the World Economic Forum, you were reportedly telling people that you were really worried about the risks inherent in the property valuations and excess leverage and the rise in oil and commodity prices. Would that be fair to say you were of that mind around January 2007? Mr. Fuld: I was clearly focused on oil, yes, sir. Mr. Tierney: Then I think we go back to the situation where we know you were in that stage in December 2007. At the end of that year, there were payments made out, both cash and stock bonuses to your employees. They totaled about $4.9 billion. So is there any thought given at that point in time to say to your employees, this isn't the time to be handing out $4.9 billion in cash. We have a liquidity issue here. We have been seeing it coming for all year long. And we are going to keep that money in the company liquidity for the benefit of our shareholders, for the benefit of the public with whom we deal, and for the economy. Mr. Fuld: At the end of 2007, I did not believe at the time that we had a liquidity problem. And our most important assets in the firm are clearly our employees. They are the ones that touch the clients every day and do business every day. Mr. Tierney: I understand. I am a little shocked. I mean, a lot of other people thought that you had a very precarious position. At the end of 2007, you thought everything was fine? Mr. Fuld: We had just completed a record year, sir. Mr. Tierney: And if you want to cover that for a second, the record year that you just completed and the reports on that had some, according to one account, had some rather aggressive and bizarre accounting practices on that. They list out four or five things that they thought were strange. You listed a 722 million dollar paper profit on level three equity holdings, stock that doesn't trade publicly; there aren't liquid markets out there. You claimed a nine percent profit on them. At the same time, Standard and Poor's index on publicly traded stocks fell by 10 percent. That was what made you seemingly have a record year. One of your short sellers, Mr. David Einhorn, said he was told by your chief financial officer that $400 million to $600 million came from writing up the value of electric generating plants in India . He thought the value was somewhere around $65 million, not $400 to $600 million. He also said Lehman showed some $600 million of profit because of the decline in the market value of your own debt obligations and sort of assimilated that to the fact that it is permissible accounting surely enough, but it is like the profit that you make when your house is foreclosed for a value that is lower than your mortgage. Last, he said another $176 million was on your books by almost doubling, to some $365 million, the value ascribed to certain mortgage servicing rights; in other words, the value you get paid for servicing mortgage holders' collection of payments and doing their paperwork, which are sort of tricky things to value. So I know that at the end of the year maybe your books looked like they were good, but if those were the reasons for that, then I think it is questionable why $4.9 billion is going out to the employees in bonuses, cash and stock, and why you are spending another $4 billion buying some of that back. And I think one of your investors here today clearly said he was horrified to find out you were doing that. That is why I raise the question. Thank you, Mr. Chairman.

Chairman Waxman: I would just note, Mr. Fuld, that in January 2008, there was a presentation to your board, on which you serve, by Eric Felder. And he said very few of the top financial insurers have been able to escape damage from the subprime fall out. And a small number of investors, accounting for a large portion of demand liquidity, can disappear quite fast. So I just want that to be on the record. I would now go to Ms. Watson. Ms. Watson: Thank you so much. And Mr. Fuld, we are so pleased that you are willing to come and sit on the hot seat and admit that you take full responsibility. We heard from the first panel's view on what caused this financial crisis. And one key factor was deregulation or inadequate regulation of big financial entities like yours, Lehman Brothers. I would like to get your view on this topic, because as a publicly owned broker-dealer investment bank, Lehman was subject to a number of SEC regulations. The company was required to report important financial information to shareholders, and you were required to meet the basic SEC requirements to make sure that you were adequately capitalized. Is that correct? Mr. Fuld: Yes, Congresswoman. Ms. Watson: And in your written statement, you explain that the SEC and Fed conducted oversight of your balance sheet. As you stated, they were privy to everything that was happening. Is that correct? Mr. Fuld: Yes, Congresswoman. Ms. Watson: But, Mr. Fuld, Lehman Brothers went bankrupt. Your investors and your creditors lost hundreds of billions of dollars. And the failure has had a widespread impact for the rest of the economy. Would you agree that the current regulatory framework and the way they were implemented in your case failed? Mr. Fuld: Are you asking specifically about the SEC? Ms. Watson: Yeah. The regulatory framework. Mr. Fuld: Specifically about the SEC? Ms. Watson: Yes. Mr. Fuld: Because I had said in my written testimony that I thought the overall regulatory system had to be redone. Ms. Watson: You will agree that they failed. Mr. Fuld: But specifically to the SEC, we had extensive dealings with the SEC. They actually had dedicated and knowledgeable people actually in our firm overseeing a number of our daily activities. I went to them, our firm went to them specifically talking about naked short selling. They were constructive and positive. We went to them with an idea of creating something that we call Spinco. Spinco was the -- was a new independent entity into which Lehman would place some number of commercial real estate assets, along with a piece of capital, and then spin that, which means give that to our shareholders, which we believed would have created true shareholder value over a longer period of time. This actually was a model that I believe could have been very helpful and instructive. Ms. Watson: Yeah, I am watching our timer there. So let me just say that we have learned how Lehman Brothers relied on an unregulated bond rating agency, whose conflict of interest gave him every incentive to rate your company's risky bonds as safe investments. We have heard how housing and banking regulators failed to curb the predatory lending abuses in the subprime market. And we have heard about how the net capital rule was implemented so Lehman and other investment banks could ramp up their leverage to dangerously high levels. And we heard that the SEC is underfunded, understaffed, and led by a chairman who either was unable or unwilling to enforce even the basic laws on the books. Do you think this deregulation and lack of oversight contributed to the melt down on Wall Street? Mr. Fuld: I cannot talk to what -- Ms. Watson: Do you think it contributed -- my time is almost up -- to the melt down on Wall Street? Mr. Fuld: I cannot talk to what the SEC did with the other firms. Ms. Watson: Do you think it contributed, or are you wholly and solely responsible for the melt down on Wall Street? Mr. Fuld: I actually gave the SEC high marks for trying to be constructive. Ms. Watson: No -- Okay. Here is my bottom line question. If all the things that I just spoke of you think were just fine and worked like they should, the regulations, then it is your total responsibility for the failure of Lehman Brothers in bankruptcy? Mr. Fuld: In retrospect, it is easy to go back -- Ms. Watson: Yes or no? Yes or no? My time is up. Mr. Fuld: If you are asking me, do I -- Chairman Waxman: The gentlelady's time is up, and Mr. Fuld, you will be permitted to answer the question. Mr. Fuld: Thank you, sir. If you are asking me, did the regulatory framework contribute, or the lack of regulatory framework, contribute to where we are today? I would say yes. And that is why I think we need to redo -- Ms. Watson: Thank you. Thank you. That is the answer I was trying to get to. Mr. Fuld: That is why I think we need to redo the regulatory framework.

Chairman Waxman: Thank you, Ms. Watson. Mr. Higgins. Mr. Higgins: Thank you, Mr. Chairman. Mr. Fuld, there appears to be inconsistencies between your public statements and the private information you were receiving internally. Let me read you some of these inconsistencies and ask you to respond. In January of this year, Eric Felder, one of your top executives, made a presentation to you and the board of directors. He talked about the company's finances, and observed that, "very few of the top financial issuers have been able to escape..." -- Mr. Fuld: I am sorry, I didn't hear that. I am sorry. After Felder, I didn't hear that. Mr. Higgins: Yeah, he talked about the company's finances. He observed that, "very few of the top financial issuers have been able to escape damage from the subprime fall out." He then warned you explicitly that in the current environment, "liquidity can disappear quite fast." But that is not what you were telling the public. In December 2007, in a press release, you said, "our global franchise and brand have never been stronger.'' My question is, why didn't you say publicly what you were being told internally, that you had to be careful because your liquidity could disappear quickly, which was in fact what happened? Mr. Fuld: Mr. Felder's presentation was when, January you said? Mr. Higgins: December 2007, January 2008. This year. Mr. Fuld: We actually listened very carefully to Mr. Felder. And I believe the record book will show that we reduced our balance sheet. We reduced our leverage. We raised capital. We increased liquidity. So we did listen. Mr. Higgins: Let me show you another internal document. This document is a document that your attorneys produced to the committee. It is from June 2008, 6 months later. This is a set of talking points describing what happened over the past year and why your company posted record billion dollar losses. This is an internal document that was never made public. And it seems to admit the truth about what was going on. It asks -- this is your internal document -- why did we allow ourselves to be so exposed? And then it spells out the reasons: "Conditions clearly not sustainable. Saw warning signs. Did not move early, fast enough. Not enough discipline in our capital allocation." But that is not what you told the public that month. Here is what you said during an earnings call with investors on June 16th: Let me discuss our current asset valuation on those remaining positions. I am the one who ultimately signs off and am comfortable with our valuations at the end of the second quarter. Because we have always had rigorous internal process, our capital and liquidity positions have never been stronger. Mr. Fuld, I don't see how you could say that. Your internal documents said that conditions are clearly not sustainable and that you did not move early or fast enough. But you told the public Lehman had never been in a stronger position. How do you reconcile your public statements with the company's internal assessments? Mr. Fuld: Was this my document? Mr. Higgins: These are documents that your attorneys provided the committee. Mr. Fuld: I didn't mean that. Is this my document? Is this a presentation that I gave? Mr. Higgins: These are documents internally that went past your desk in the past 6 months. Mr. Fuld: This document does not look familiar to me. And if it was an internal document, it was -- I really can't speak to that, because this document is not familiar to me. Mr. Higgins: Well, these documents were made -- Mr. Fuld: But if you tell me it is mine, I believe you. Mr. Higgins: And ultimately, you are responsible. And this inconsistency with public statements made conveying a strong position and internal documents showing a direct contrast to that assertion, I think, is very troubling with respect to the issue of trust and confidence. According to your lawyers -- Mr. Fuld: I am looking very carefully at this -- Mr. Higgins: -- This is a document that you either wrote or you reviewed. Mr. Fuld: I am looking at this very carefully, sir. It does not look like my document. Nor does it look like a speech that I gave. Nor does it look like anything that I reviewed. Mr. Higgins: These are your documents. Mr. Fuld: Excuse me, sir? Mr. Higgins: These are your documents.

Chairman Waxman: The gentleman's time has expired. Mr. Shays, you wish to yield 2 minutes to Mr. Mica. Mr. Mica: Let me get down to some of the heart of this. I guess a lot of the collapse occurred on September 9th and 10th. You were trying to find $5 billion to back up your transactions. I recommend to everybody the Wall Street Journal today. They did an excellent job, better than the committee, of going through some of the public and private statements. I wouldn't necessarily pay for it. Maybe you could get it online. It is two bucks. But it does outline what you were going through. One is J.P. Morgan asked you for the $5 billion. Lehman executives claimed that they had a restructuring plan. And then you had discussions that night. You wanted to go into a conference call. Your counsel said not to go into a conference call. Maybe you could tell us about that. On the 10th, however, you told investors, we are on the right track to put these last two quarters behind us. Now, people want to know if you defrauded investors -- I mean, I am going to be blunt here -- by coming out and saying that as opposed to what happened on the 9th, and you knew or were told you weren't going to get the money. Mr. Fuld: As I said before, I am not -- I am not really sure when that conversation -- Mr. Mica: Yeah, but you had to know at some point you weren't going to get the $5 billion. I mean the Korea -- the attempt to get the money from Korea was -- Mr. Fuld: I am sorry, I thought you were talking about J.P. Morgan. I apologize. Mr. Mica: Okay. But you were trying to get the money -- well, J.P. Morgan wanted the money, and you were trying to find the $3 billion to $5 billion, right, to keep the ship afloat. Mr. Fuld: Two very different things. Very different things. Mr. Mica: Well, this is on the 9th. Mr. Fuld: Well, J.P. Morgan, as I said before, in answering one of the other questions -- Mr. Mica: On September 9th, you needed $5 billion to keep the ship afloat. You were told, and your counsel told -- also advised you not to go ahead with the conference call to disclose this internally. But you came out on the 10th and said, we are on the right track to put these last two quarters behind us. That is what you said. Again, I am just reporting -- Mr. Fuld: Correct. In our September 10th analysts call, I firmly believed that we put the last two quarters behind us. We had done a tremendous amount -- I don't want to go through the whole thing all over again -- but lowered our leverage, raised capital; you heard it all before. I am not going to go through it again. Mr. Mica: Were you told the night before you weren't going to get -- be able to cook the deal? Mr. Fuld: I don't know what that refers to. Mr. Mica: Getting the money to keep the Lehman ship afloat. Mr. Fuld: What we said on September 10th was that we had adequate capital. We talked about a plan that involved spinning off those commercial real estate assets and that we were going to have to put capital into that. On the call, people talked about, how are you going to fill that? We talked about the sale, potential sale of IMD, either all or some, which would have created $3 billion of tangible equity. I think if you go back and look at the third quarter announcement, you will see that. Possibly more if we had sold it for a higher price. We had plans at the time to go to some of our preferred holders and convert some of those preferreds to equity. Because we had to prerelease because of the rumors about our company, we didn't obviously have a chance to complete some of those plans. We didn't know how much capital we were going to need to equitize Spinco. We didn't know how much of the commercial real estate assets would be sold. But that was all 3 months out. On that Wednesday, we had $41 billion. We had plenty of capital to operate. All conversations about additional capital were about what we were going to do when we took capital and put it into the new Spinco. That was all 3 months out. And that was obvious to shareholders. That is what we were talking about. And there were a number of questions from analysts at that time about that. So there was disclosure about where we were and, I believe, understanding. And there certainly was no attempt to mislead anyone. Mr. Mica: Again, again, before the committee, under oath, the night before September 10th, when you made that statement, did you in fact know that you weren't going to get the estimated $3 billion to $5 billion to keep the ship afloat? Mr. Fuld: Congressman, again, I say I am sorry, those are two very different numbers. One is additional collateral for our clearing bank. I know you are looking for an answer here. That is not capital. That is collateral. Two very different things. We believed we were going to raise, "that $5 billion, by either selling all or part of Investment Management or the sheer fact that we were going to spin those assets off, then we didn't need that much capital." The $5 billion was additional collateral that J.P. Morgan was asking for.

Chairman Waxman: The gentleman's time has expired. The Chair now recognizes Ms. McCollum. Mr. Fuld: Did I answer that, though, for you, sir? Ms. McCollum: Mr. Chair, a point of personal privilege. Chairman Waxman: Yes. Ms. McCollum: How I would go about yielding to the gentleman from Tennessee so he could make a flight? Chairman Waxman: I didn't hear you. Ms. McCollum: How I would go about allowing time for the gentleman from Tennessee to go ahead of me so he could catch a plane? Chairman Waxman: Then why don't I just recognize him now? Mr. Cooper: I thank the Chair. Mr. Fuld, in your testimony, on page 8, you say what happened to Lehman Brothers could have happened to any firm on Wall Street and almost did happen to others. But it didn't happen to the others. There is a difference. And you cite many factors in your testimony about how it could have been different, you know, if regulators had behaved differently or different things had happened. What could you have done differently personally that might have changed the fate of Lehman Brothers? Mr. Fuld: With the benefit of hindsight, sir, going back a couple of years, I would have made some changes to how we looked at and thought about our mortgage origination businesses, our commercial real estate business, and probably our leveraged loan business. Those were three of the areas that over the second and third quarter created some losses. And I believe in my verbal testimony I said, given the opportunity to look back, I would have done things differently. Should I have closed those businesses down then, I think people would have looked at me and said, that's irrational to have done that. But knowing what I know today, that clearly could have been a smart move. But given the information that I had, that is not the decision I made. Mr. Cooper: Well, that was a decision you could have made two or three years ago. Given your book of business in 2007 and 2008, were there decisions you could have made to have changed the destiny of Lehman Brothers just in the immediate past? Mr. Fuld: We did make aggressive decisions to close some of the mortgage origination businesses. We had substantial hedges on our residential mortgage positions. In retrospect, I think we were slower on commercial real estate. I, like a number of other people, thought the mortgage crisis was contained to residential mortgages. There were a number of people, many experts included, that also thought that. And I was wrong. Looking back now at that information, I thought it was contained. We thought it was contained. And experts thought it was contained. Mr. Cooper: You mentioned being, ``slow on commercial real estate.'' Does that mean correctly valuing the portfolio of commercial real estate properties? Mr. Fuld: No, sir, it does not mean anything about valuation. It means about how quickly we thought about disposing those assets. And I think the record book will show that we went from $50 billion of those assets to $30 billion, keeping the remaining -- I shouldn't say keeping, but ending up with $30 billion that would go into -- either 30 or less, depending upon how much of the remaining 30 we sold in the fourth quarter, the remaining piece going to Spinco to be spun to our shareholders, which we firmly believed had real value. Mr. Cooper: You had a committee, the finance and risk management committee, which I believe was chaired by the once legendary Henry Kaufman, a previous panel said that this committee only met twice a year in 2007 and 2006. Were they giving you advice on these long-term strategic directions? Mr. Fuld: Let me just clarify one thing, if I may. I believe they did meet twice in 2007, but they met four times this year so far. Well, it is over now, so it is four times this year. Mr. Cooper: Were they giving you advice on changing strategic direction for the firm? Mr. Fuld: We talked about assets, and not just at the risk and finance committees, we talked about it at the board. We talked about how we were bringing down our exposures on residential and on commercial and on leveraged loans at almost each and every board meeting. Whether it was the risk committee or finance committee, we talked about it. It was clearly a subject on everybody's mind. Keep in mind that this was a board that did have a lot of financial experience. This was a strong, independent board. I was the only Lehman person on the board. These people -- some of these people ran banks, IBM, other companies, Celanese. These were experienced people. And they had never any reservations about giving me advice and having a view about the markets.

Chairman Waxman: Thank you, Mr. Cooper. Your time has expired. Ms. McCollum. Ms. McCollum: Thank you, Mr. Chairman. And I thank the committee for allowing Mr. Cooper to move forward. My constituents in Minnesota understand that you don't have to do something illegal to do something wrong. Imperfect Federal regulation isn't a license for unethical behavior, especially when it puts taxpayers at risk. In our current regulatory framework, there is a gray space between legal activity and illegal activity. And in that space, financial firms can make a choice to either obey the letter of the law but not to honor the spirit of the law. Twelve years ago, and you have been with the firm for 42 years according to your testimony, Lehman Brothers Holding, Inc., sent a vice president to California to check out First Alliance Mortgage. Lehman was thinking about tapping into First Alliance Mortgage's lucrative business of making subprime loans. The vice president, Eric Hibbert, wrote in a memo describing First Alliance as a financial sweat shop, specializing in high pressure sales for people who are in a weak state. First Alliance, he said, the employees, "leave their ethics at the door." The big Wall Street investment bank, that was Lehman Brothers, decided First Alliance wasn't breaking any laws, and Lehman went on to be, to lend the mortgage company -- they needed about $500 million worth of sells and more than $700 million worth of bonds. In other words, Lehman Brothers is an example of how Wall Street's money and experience could have been used to prevent us being in this subprime mortgage crisis. History: We should learn from it. You, in your statement, on page 5, you said, "we did everything we could to protect the firm.'' So I go back to this memo that Mr. Bishop had up and ask you if you agree with the spirit of the memo. Why did we allow ourselves to be so exposed? Did you ask those questions? Did you reflect that conditions were clearly not sustainable? Did you see warning signs? Did you move fast enough? And I ask that because of two things that have come to my attention, that the Federal Bureau of Investigation has launched preliminary inquiries as to whether or not Lehman or its executives committed fraud by misrepresenting the firm's condition to investors. So, sir, I want to ask you some questions. On September 10th, 5 days before your bankruptcy filing, you and your chief financial officer, Ian Lowitt, held a conference call for investors. According to the Wall Street Journal, you were advised by your bankers not to hold this call because there were too many open questions. It is my understanding that at the time you did make the call, and that you were frantically trying to raise capital either through new investors or selling off assets. So when you and Mr. Lowitt spoke to your investors and said that you did not need more capital, and that Mr. Lowitt said to investors when asked whether Lehman would need to raise $4 billion, I am paraphrasing, ``we don't feel that we need to raise that extra amount. Our capital position at the moment is strong.'' So, sir, is this accurate? Were you told not to hold the call? Were you trying to raise capital during the week before you filed bankruptcy? Is it an accurate statement that your capital position was strong on September 10th? Mr. Fuld: It is correct that our capital position on September 10th was strong. Ms. McCollum: Did anyone tell you, advise you against holding the conference call I referred to? That should be a yes or no, sir. Mr. Fuld: Well, you are asking me -- did anyone? Ms. McCollum: So that's a pretty big call that was made -- Mr. Fuld: Yes. Ms. McCollum: -- Five days before filing bankruptcy, and your chief financial officer was present on the call. I ask you, did any of your outside bankers or other advisers warn you against making, holding this call? Mr. Fuld: I had so many conversations, I would never say to you that no one -- Ms. McCollum: Well, sir, maybe you remember. Were you trying to raise capital during the week before you went bankrupt? Mr. Fuld: The week before, 2 weeks before, 3 weeks before. Ms. McCollum: Sir, I asked you a week before. I was just asking you for the week before this. Mr. Fuld: I am saying yes to all. Ms. McCollum: You are saying yes to all. When you were raising that capital, no one in your firm -- Mr. Fuld: Yes. No, no, let me finish. I would like to finish because there's a different piece to that. What we were looking to do was to raise capital after we completed -- Ms. McCollum: You were raising capital. Mr. Fuld: Excuse me, please -- after we completed the spinoff, which would probably have been January. After we had completed the spinoff of the commercial real estate assets. On September 10th, we had a strong capital position. We were trying to anticipate how much capital we were going to put into Spinco, how much capital we were going to use. We were trying to anticipate how much we would sell the investment management division for. So there were a number of moving pieces. But on September 10th, given the business that we had, we had sufficient and strong capital and liquidity.

Mr. Tierney [now presiding Chair]: Thank you, Mr. Fuld. Thank you, Ms. McCollum. Mr. Van Hollen, you are recognized for 5 minutes. Mr. Van Hollen: Thank you, Mr. Chairman. Mr. Fuld, you said earlier in your testimony that at Lehman Brothers when things were going well then people would do well. When things weren't going so well, then people would have cutbacks. I have to say that I think people looking in have concluded, based on the compensation structure, that when things went well people did really well. When things didn't go well, they still did very well. I would like to call your attention to a memo that was written on September 11, 2008, just 4 days before Lehman Brothers declared bankruptcy. And I hope someone can provide you with a copy of the memo. It's a proposal from the compensation committee, you are cc'd on the memo. It talks about compensation for two employees of Lehman Brothers. One was Andy Morton, I assume you recognize that name. Mr. Fuld: I do, sir. Mr. Van Hollen: He was the previous global head of fixed income. It said, the document here says he was involuntarily terminated. The memo here proposes to give him an additional $2 million cash payment. The other official mentioned in the memo is Benoit Savoret. I assume you know him as well, is that right? Mr. Fuld: I do indeed, sir. Mr. Van Hollen: He used to be Lehman's chief operating officer of Europe and the Middle East until he was terminated. He was also, according to this memo, involuntarily terminated. Yet this memo proposes to give him a $16 million cash payment, again, just days before Lehman Brothers declared bankruptcy. These are two individuals who were involuntarily terminated. I think the normal sort of parlance is fired. Yet they are being given, combined, about $20 million in additional compensation, despite the obvious poor performance at this point, which nobody can deny. I ask you, is that appropriate? I mean, we are here having this conversation with you and the American people. Is that appropriate that 4 days before Lehman Brothers declares bankruptcy, that two individuals who have certainly been part of the decisionmaking that led to the decline would be given $20 million in additional compensation? Mr. Fuld: There were two pieces to that, clearly, Andy Morton and Benoit Savoret. Andy Morton was given, I think it's $2 million. Mr. Van Hollen: Yes. Mr. Fuld: We felt that was -- or, more importantly, the compensation committee felt that was appropriate for his years of service. The $16 million, $16.2 million, was not a severance payment. The $16.2 million was a contractual obligation that the firm had made to Mr. Savoret. I forget when it was, but it was earlier in the year. That contract said that at any time if terminated he was due the items of the contract. So that's what that was. That was not a severance payment, sir. Mr. Van Hollen: Regardless of his performance, he would be due that amount of money is what you are saying, under the contract? Mr. Fuld: Unless he was fired for -- Mr. Van Hollen: Let me ask you this. You would agree, would you not, that people can make decisions that in the short term maximizes profits and bonuses but are bad decisions for the long term? I mean, there are decisions that can maximize short-term profits, but people would also agree that they might not be the best long-term interests in the company; isn't that right? Mr. Fuld: If you are referring to this gentleman? Mr. Van Hollen: No, I am just referring as a general proposition. You would agree that there are times when you can maximize short-term profits, but if you looked at over the longer term, people would agree it's not a good, long-term decision. You would agree that there are some decisions that fall into that category? Mr. Fuld: Certainly not by design, but in retrospect, clearly. Mr. Van Hollen: Let me ask you about clawbacks. I am not talking about anything with respect to Lehman Brothers, but just as a proposition. Wouldn't you agree that it's appropriate that if somebody makes a decision that raises short-term profits and, therefore, bonuses, but then it's later shown that those same decisions resulted in harm to the company, that on behalf of the shareholders and certainly in cases where the public is now involved, that the shareholders or the public should be able to go back in and get a clawback and take those bonuses or additional payments back that are proven, with the benefit of hindsight, to have been bad decisions for a company and the shareholders? Mr. Fuld: That was actually one of the things I spoke about when I said interesting way to go forward is a long-dated compensation system. In our case, that's exactly what we had. We had a long-dated compensation system. Look, I am not proud of the fact that I lost that much money. But it does show that the system, our compensation system, did work. It left 10 million shares plus a whole number of options. I say, I am not proud of that. But when the firm did not do well, I was probably the single largest individual shareholder. I don't expect you to feel sorry for me. I don't mean that. That's not my point. My point, though, is that the system worked. Mr. Van Hollen: Mr. Chairman, if I could, you are now referring to shares that you owned which, obviously, when the company went bankrupt, went down. I am also referring to bonus payments that may have been made in previous years to executives, including yourself, when, now that the company has gone bankrupt, wouldn't it make sense to have provisions to protect shareholders, not just to -- clearly, when the shares go down, the value of the company goes down, the share values do. But wouldn't it make sense to have clawback provisions with respect to bonus payments, cash payments? The shareholders could recover those moneys that were bonuses for what clearly proved to be bad decisions? Mr. Tierney: If you could answer that briefly, Mr. Fuld. Then we will move on. Mr. Fuld: I am sorry, sir. Mr. Tierney: If you want to answer that briefly, you may, but we have to move on. Mr. Fuld: Our compensation system was specifically set up, even for me. In 19 -- I am sorry, in 2007, 85 percent of my compensation was in stock. I lost that. All stock that I got for the last 5 years, I lost that. Actually, compensation that I received back from 1997, 1998 and 1999, I went to the compensation committee and said I believe we should extend the vesting on this. I could have gotten it 7 years ago. I went to the compensation committee and said this should be extended to a 10-year vest. I lost all of that. I would like also for this committee to know that before the end of our second quarter, I went to my board, and I said, I think we are going to have a tough quarter. We were talking about how we were going to pay the troops, as I called it. I said I want you to take me out of it. I believe, given this performance, my recommendation to you, is that I do not get a bonus. I would like this committee also to know, I got no severance, I got no golden parachute. I had no contract. I never asked for a contract. I never sold my shares. That's why I had 10 million, because I believed in this company. I believed that this company -- and that's why I said, I am glad I got these last two quarters behind us. I believe we are on the right track. I could have sold that stock. I did not, because I firmly believed that we were going to return back to profitability and get back on the road.